- News

- Business News

- India Business News

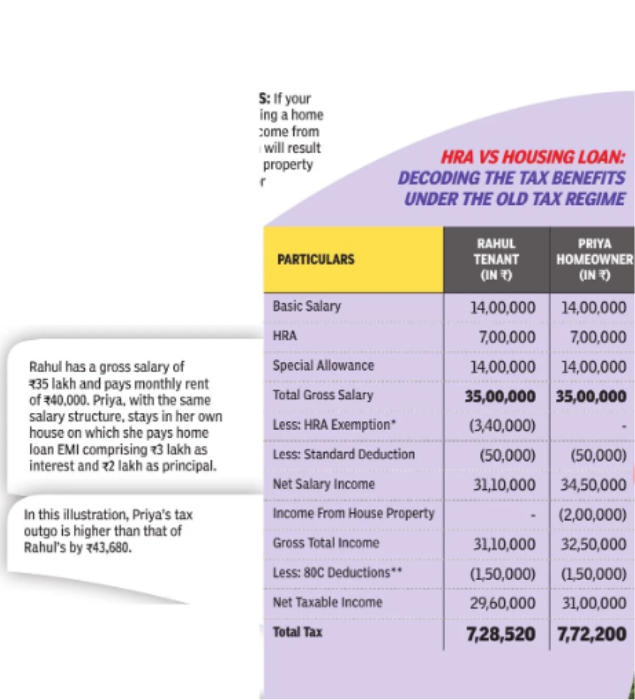

- Union Budget 2026: To rent or to buy... what's the best move?

Trending

Union Budget 2026: To rent or to buy... what's the best move?

.

Budget 2026

- A house is an asset and EMIs go towards creating this asset

- Tax benefits available on home loans

- Heavy upfront costs such as down payment and registration, followed by property taxes and repairs

- House properties are illiquid as they cannot be sold quickly

- Property prices see fluctuations and may not fetch expect ed returns

- EMIs have to be paid regularly, irrespective of situations like loss of income

End of Article

Follow Us On Social Media

Hot Picks

Top Trending

Tired of too many ads?go ad free now

Trending Stories

In Business

Entire Website

- Union Budget 2026: Be a goal and skip the investment penalty

- Union Budget 2026: Tension & sanctions show in aid card

- To rent ot to buy... what's the best move?

- How new labour codes have shifted goalposts

- Budget 2026: Buy back proceeds will be taxed as capital gains for shareholders, but promoters pay an extra price

- Retrospective clarifications on re-assessment and invalidation of tax orders

- Stock market today: Nifty50 opens flat; BSE Sensex down over 100 points after Budget day crash

- Union Budget 2026: India Semiconductor Mission 2.0 sets ground for AI jump

- Launch Of Mahatma Gandhi Gram Swaraj Scheme: FM unveils new rural push; opposition protests MGNREGA renaming

- Divyangjan Kaushal Yojana: Govt unveils new schemes for PwDs; Rs 300cr set for training, devices

- Union Budget Speech 2026 Live: What time is Nirmala Sitharaman’s speech today?

- Pakistan refuse to play India: Govt bars T20 World Cup clash - timeline

- Exclusive | Rashid Latif on Pakistan boycotting India match: ‘In 24 hours, anything is possible'

- After 'ek rupiya bhi nhi kamaya' remarks, boxing legend Mary Kom issues apology video - Watch

- Pakistan Boycotts India Match: ICC calls move a serious concern; warns of long-term impact

- ‘Hum kuch nahi kar sakte’: Pakistan captain breaks silence on boycotting India match at T20 World Cup

- “I needed to let him go”: Dwyane Wade’s wife Gabrielle Union breaks silence on how she wanted to end their marriage over her fertility issues

- MLB trade rumors: Los Angeles Dodgers reported to sign $400 million Cy Young in a blockbuster deal with the Detroit Tigers; Roki Sasaki key trade asset?

- Why Travis Kelce and Taylor Swift skipped the 2026 Grammys amid personal priorities and leaked texts drama

- Cam Skattebo’s offseason break heats up as girlfriend Chloe Rodriguez makes waves with daring Cabo look

Financial calculators

Tired of too many ads?go ad free now

Explore Every Corner

Across The Globe

Budget 2026Cam SkatteboCharlie KirkSuper Bowl HalftimeSalman Ali AghaDeshaun WatsonMary KomRashid LatifT20 World Cup 2026Carlos AlcarazBudget Speech LiveStock Market TodayGold Silver PriceEducation Budget 2026Budget HighlightsSnoop Dogg DaughterBudget Cheaper and CostlierStock Market CrashEducation BudgetDefence BudgetNew vs Old Tax RegimeBudget for NRIKayla NicoleTerence CrawfordMinnesota Timberwolves vs Memphis Grizzlies InjuryGiannis AntetokounmpoGisele BndchenSuper Bowl Coach Bruce AriansTravis KelceT20 World Cup 2026 Schedule

Hot on the Web

Amitabh BachchanRanveer SinghWill SmithThe 50The 50 Contestants ListRam CharanMardaani 3 Box Office CollectionFlying UmbrellaJana NayaganDon RitchieInternational VisaDhurandhar OTT ReleaseRani MukerjiBorder 2 CollectionAnke Gowda StoryNelson DilipkumarBorder 2 Movie ReviewArijit SinghBrain CancerShyam PathakRobert BrowningNortheast DishesFebruary 2026 Horoscope PredictionsSeneca QuoteBhoot Police 2Purnima 2026Sunaina RoshanPadayappa 2Dhurandhar Movie ReviewChandra Grahan 2026William ShakespeareWorld Largest Late Roman HoardPink DolphinsTim CookQuote Of The Day By Richard FeynmanMadagascar SpiderAnime Paradox CodesAndrej KarpathySam Altman QuoteAsteroid 2024 YR4 May Hit MoonRaven Bird

Trending Topics

ICC T20 World CupDelhi Capitals WPL 2026IGNOU January Re RegistrationHSSC Recruitment 2026MBA Finance vs MarketingBanking Sector BudgetNirmala Sitharaman SpeechBudget 2026 Income TaxUS government shutdownTirupati laddu gheeKDMC mayor raceBareilly flyoverCJ RoyKolkata godown fireGhaziabad stabbingDefence Budget 2026Section 87ABudget full textNew income tax slabStock market crashBudget STTHealth Budget 2026Trump’s tariffsIndia-US trade dealUS Department of EducationFederal Tax Credit ProgramMyles GarrettPortland Trail Blazers vs New York KnicksH 1B Visa AbuseIncome Tax CalculatorMahindra Xuv 7xoHyundai ExterPhoebe GatesElon MuskNyt ConnectionsSemiconductor Mission 2.0Realme P4 PowerImf Data Shows India Above AmericaElon MuskWordle TodayBest Camera Phones Under 30000Auto News

Popular Categories

HeadlinesSports NewsBusiness NewsIndia NewsWorld NewsBollywood NewsHealth+ TipsIndian TV ShowsTechnologyTravelEtimesHealth & FitnessChinese Horoscope PredictionsMarketsAstrologyAutoWeather TodayGold Rate Today DelhiSilver Rate TodayPlatinum Rate TodayIs Bank open todayBank Holidays in February 2026Public Holidays in February 2026DeorhiNFL ScheduleTechnology NewsInternational SportsPublic HolidaysBank Holidays

Trending Videos

How and why India can create history at T20 World Cup | Message for coach Gambhir‘Failed Intimidation Tactics’: Cuba Under Fire As US Says Havana Harassed Diplomat Mike HammerShots Fired Outside Rohit Shetty’s Bungalow In Mumbai, Cops Detain FiveChagos Islands Plot Twist: Unexpected Challenger Shocks Trump Amid UK Feud | DETAILSKristi Noem Admits DHS “Messed Up” in ICE Operations Amid Impeachment Threat? | WATCH‘Liam Is Home!’: 5-Year-Old Boy, Father FINALLY Freed From Texas ICE Centre After Minneapolis RaidLos Angeles Erupts In Riots; Scores Clash With Police, Blast ICE Ops | Streets On Fire | WatchTrump Dimisses Khamenei's Regional War Threat; Expects Deal With Iran | WATCHRussia Savagely Mocks Trump After 'Hollow Nuke Threat' | 'Where Are Your Submarines, Donald?''DEATH TO AMERICA': Iranian Parliament Designates European Armies As Terrorist In Tit-For-Tat MoveTrump Says New Epstein Documents “Absolve” Him And Hints At Legal War | WATCHFULL: Khamenei's Roaring Warning To U.S. And Israel Amid Iran War Threat | 'Will Crush...''Europe About To Lose Greenland?': Lavrov Hammers EU; Admits Differences With US., But Says Trump...Andrew Sent Family Pictures Of His Daughters To Epstein, Shocking Documents Exposed | WATCHKCR, KT Rama Rao Thank Workers As SIT Probes Phone Tapping AllegationsPM Modi Meets Sant Niranjan Das, Attends Sant Ravidass Jayanti In Jalandhar‘We’re On The Same Page’: Shashi Tharoor After Meet With Rahul, KhargeUnion Budget 2026 Is Wholesome, Women-Focused: Kangana Ranaut

Latest News

Ramadan 2026: Will the Islamic month of fasting begin from Wednesday, February 18 or Thursday, February 19?Union Budget 2026: Tension & sanctions show in aid cardGrammys 2026: Trevor Noah roasts Nicki Minaj and Donald Trump; says, 'She's discussing very important issues'Caitlin Clark breaks silence on WNBA-CBA negotiations in her broadcast debutTo rent ot to buy... what's the best move?Ranji Trophy: Ayush Doseja caps debut season with match-saving 159 for Delhi vs MumbaiFM: Hike in transaction tax to check F&O speculationPavitra Punia postpones her wedding with US-based businessman after family emergencyApple may launch foldable iPhone in 2026, offering design similar to Samsung Galaxy Z FlipHow new labour codes have shifted goalpostsQuote of the day from Bhagavad Gita: "Man is made by his belief. As he believes, so he is"UP man strangled to death by wife, her family over financial dispute; body staged as suicideWPL: Delhi Capitals beat UP Warriorz by 5 wickets to reach EliminatorBudget 2026: Buy back proceeds will be taxed as capital gains for shareholders, but promoters pay an extra priceWho is Caitlin Clark's inspiration? WNBA athlete reveals her star player from NBA during Sunday Night BasketballStock market today: Nifty50 opens flat; BSE Sensex down over 100 points after Budget day crashMBA in Finance vs. Marketing: Which specialisation offers better opportunities?Buck for the bang: Post Operation Sindoor, defence bags its biggest hike

Copyright © 2026 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service