- News

- City News

- mumbai News

- Little Master scores big in I-T tribunal dispute

Trending

This story is from January 28, 2017

Little Master scores big in I-T tribunal dispute

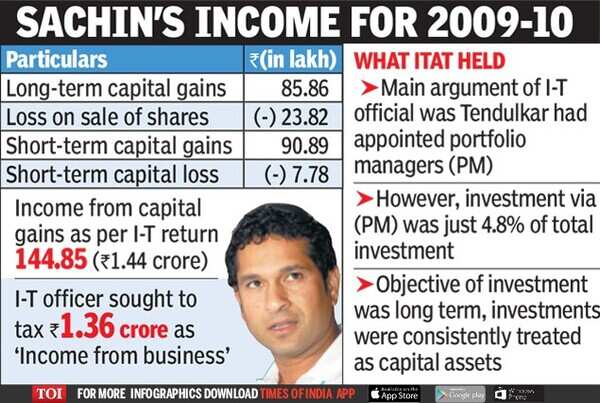

The little master, Sachin Tendulkar, has scored big in an appeal before the Income-tax Appellate Tribunal (ITAT), which adjudicates tax disputes.

, which adjudicates tax disputes. <br></p>")

<p>The little master, Sachin Tendulkar, has scored big in an appeal before the Income-tax Appellate Tribunal (ITAT), which adjudicates tax disputes. <br></p>

I-T is assessed under various heads such as salary income, capital gains or income from business.

The I-T officer took this position as Tendulkar had availed the services of portfolio managers for making investments and paid them a fee of Rs 52 lakh. This, according to the I-T officer, "was not an ordinary thing for a normal investor." As Commissioner of I-T (Appeals) ruled in favour of the cricketer, the I-T department filed an appeal with the ITAT. The tribunal of members Mahavir Singh and Ashwani Taneja noted that the major income arising in Tendulkar's hands was from sports endorsements. The investment in shares was made from a long term point of view, mainly to earn dividend and maximise wealth from appreciation in value of shares. Besides, he had not borrowed money for the purpose.

Further, investment in shares via portfolio managers was only 4.86% of total investment portfolio. Tendulkar had always treated his investments as capital assets.

About the Author

Lubna KablyEnd of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In City

Entire Website

- Who is Anura Kumara Dissanayake, Sri Lanka's new president

- Early-century Lord Ganesha, Buddha statues: Images of stolen antiquities US handed over to India during PM Modi's visit

- 'My daughter would have been dead by now': When a ‘monkey attack’ in UP foiled man’s bid to rape 6-year old girl

- 'Will kill them and ...': Israel, Hezbollah vow to intensify cross-border attacks

- Ex-Google employee looking for job in Canada: “I've been reducing my India experience on my resume because …”

- How India prices of iPhone 16 series compare with that in the US, Canada, Singapore and Dubai

- 'Detonators' put on way of Army train set off alarm

- Garena Free Fire MAX redeem codes for September 21, 2024: Win free pets and vouchers today

- Intel's biggest-ever restructuring: Read the complete memo sent by CEO Pat Gelsinger to employees

- US Space Force to help set up semiconductor plant in India

- Watching, downloading child pornography are offences under POCSO Act: SC

- Atishi takes charge as Delhi CM, places empty chair for Arvind Kejriwal

- Why Project Cheetah's biggest successes are also its biggest worry

- 'Laapataa Ladies' is India's official entry for Oscars 2025

- Virat Kohli's 'bat chahiye?' moment: Akash Deep shares story

- Congress, other casteist parties only remember Dalits during their bad days: Mayawati

- Why HC stopped govt's attempt to muzzle independent media

- iPhone 16 series record sales on Day 1 in India, could help Apple to set milestone

- Sri Lanka gets Leftist prez, India a challenge in a man it’s not acquainted with

- Shots fired outside Gardens Galleria Mall in Noida, 3 arrested

Popular Categories

Hot on the Web

Top Trends

Radhika GuptaYahya SinwarRishabh PantIsrael Hezbollah WarPakistan Bomb BlastAnura Kumara DissanayakeJetblue Flight Emergency LandingPM Modi with Tech CEOAwadhesh PrasadUGC NET Result LiveBengaluru Mahalakshmi MurderRohit SharmaStolen Antiquities USShoaib AkhtarTirupati LadduPM Modi US VisitLive Cricket Score

Trending Topics

Aishwarya RaiZodiac SignsBigg Boss 18 PromoThe Great Indian Kapil ShowChia SeedS ShankarOptical IllusionSharp Eye TestChiranjeevis FarmhouseSana KhanDevaraStree 2 CollectionAnupam MittalHealthy RaitasUrvashi RautelaColdplay India tour 2025Best Laptops For CodingPM Narendra ModiAnupam MittalWordle Answer

Living and entertainment

Latest News

EC team in Jharkhand to review poll preparednessElon Musk's SpaceX to send uncrewed Starships to Mars by 2026: “One of my biggest concerns right now..”Commonwealth Master's Scholarship application open for Sept 2025: Check benefits, eligibility and how to applyGhosts Season 4: Premiere date, plot, and cast revealedWhat is the 30-30-30 weight loss method? How to do it for maximum benefits?Mom's everyday tips were a must for golden boy D GukeshYudhra Box Office: Siddhant Chaturvedi starrer earns only Rs 8.60 crore over the weekendKaun Banega Crorepati 16: Amitabh Bachchan praises Ujjwal’s resilience as he attempts the 1 Crore questionGen-Z slang words explained: 30 terms you need to knowThe truth about sugar substitutes: Safe alternative or hidden health risk?Decomposed body of civil services aspirant found in Delhi'I will come to any of your houses and start living with you': Arvind Kejriwal tells Delhi people at Janta Ki AdalatGemini, Daily Horoscope Today, September 23, 2024: Face financial strain today with expenses outpacing incomeBMC issues fresh ad for eligible candidates for nearly 2,000 clerk postViral video fact-check: Snake biting raw tomatoes in farms makes them poisonous?Aishwarya Rai set to take the Paris Fashion Week by storm; reaches the venue with daughter Aaradhya Bachchan - WATCH videosRajinikanth reacts to 'Vettaiyan' audio launch success and the viral hit of 'Manasilaayo'Margot Robbie strolls with baby bump, following 'The Sims' film adaptation news

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service