- News

- Business News

- India Business News

- Stick to a few bond funds

Trending

This story is from July 30, 2018

Stick to a few bond funds

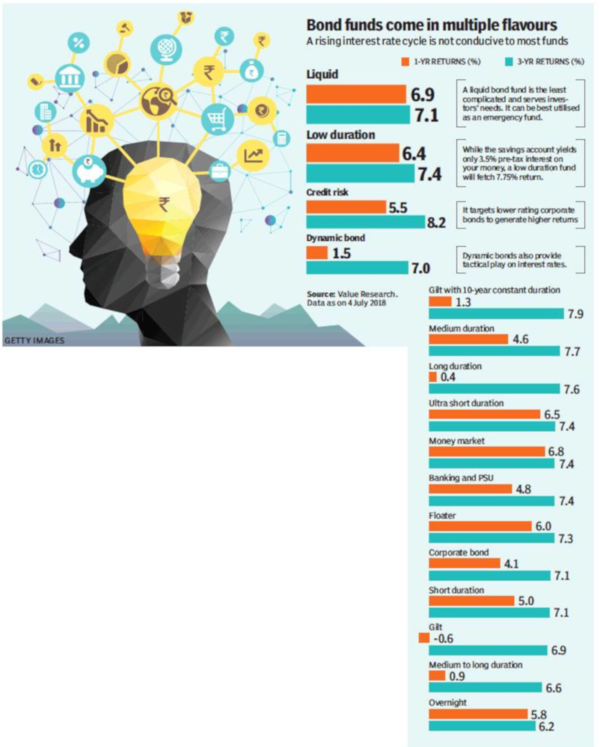

For most mutual fund investors, bond funds can seem confounding. And with Sebi introducing 16 categories of bond funds as part of its recent scheme rationalisation exercise, matters have become even more complicated. So which among these funds are the must-haves?

Representative image.

NEW DELHI: For most mutual fund investors, bond funds can seem confounding. And with Sebi introducing 16 categories of bond funds as part of its recent scheme rationalisation exercise, matters have become even more complicated. So which among these funds are the must-haves?

To choose the right bond funds, investors must understand what purpose they serve in the portfolio.

However, it is advisable to take a simplistic approach while building a bond fund portfolio, say experts. Investors need not look beyond two to three types of schemes.

A liquid fund also allows the investor to redeem the money by the next working day. A handful of schemes even facilitate instant redemption up to a limit of ₹50,000 a day or 90% of the fund value, whichever is lower. This instant liquidity puts the liquid fund on par with a savings account. These funds can also be used when staggering investment into an equity fund using the systematic investment plan (SIP). It allows you to fetch a higher return compared to using a savings account to transfer the money.

The bread and butter portion of the bond portfolio should be in a low or short duration fund, says Kaustubh Belapurkar, Director, Fund Research, Morningstar Investment Advisor. These will invest in instruments with duration up to three years, and are suitable for investors looking to park money over a similar time horizon. These are not too exposed to interest rate risk as they carry low duration in their portfolio, yet are able to capture slightly higher return compared to a liquid fund.

Amol Joshi, Founder, PlanRupee Investment Services, says, “These funds provide the best of both worlds—yielding slightly better return while largely keeping volatility at bay.” For most investors, this combination of liquid fund and low duration fund is enough to fill the bond fund basket. Their returns are least affected by the changing interest rate scenario and carry little default risk.

Other categories of bond funds, however, require a deeper understanding of interest-rate risk, duration calls and credit risk. But if investors are keen on slightly higher return, then experts suggest rounding off the debt fund portfolio with a small allocation to a credit risk fund or even a dynamic bond fund. A credit risk fund generates higher returns by targeting lower rated corporate bonds carrying a higher coupon rate.

Currently, with corporate earnings recovery on the horizon, there is a higher possibility of lower rated paper getting upgraded, which can boost the returns from a credit risk fund. However, funds with poor credit profile can take a hit if companies default on loan repayments.

For the risk takers, a dynamic bond fund can provide another tactical play on interest rates. It attempts to capture higher return by aggressively shifting the portfolio between short and long duration according to expected movement in interest rates. Theoretically, these are ideal for investors who don’t have the understanding to take a call on interest movements. Yet, most dynamic bond funds have failed to live up to the billing and have often been caught on the wrong foot, hurting fund returns.

Other categories such as medium duration, long duration, corporate bond, banking and PSU fund, among others, can be safely ignored as they usually do not add much value to the lay investor’s portfolio.

To choose the right bond funds, investors must understand what purpose they serve in the portfolio.

At the basic level, a bond fund is a cushion for the entire portfolio, meant to deliver steady returns. Vidya Bala, Head, Mutual Fund Research, FundsIndia, says, “Debt funds are meant to hedge exposure to more volatile asset classes.”

However, it is advisable to take a simplistic approach while building a bond fund portfolio, say experts. Investors need not look beyond two to three types of schemes.

The first choice should be a liquid fund, which invests in instruments with maturity of up to 91 days and it is the least complicated among all bond funds. “The returns are predictable, it lends stability to your portfolio with no accompanying credit or interest rate risk,” says Bala. Experts say a liquid fund is best utilised as an emergency fund, where one can park a part of one’s surplus cash instead of keeping the entire sum idle in the savings account. While the savings account yields only 3.5% pre-tax interest on your money, a liquid or low duration fund will fetch 7-7.5% return.

A liquid fund also allows the investor to redeem the money by the next working day. A handful of schemes even facilitate instant redemption up to a limit of ₹50,000 a day or 90% of the fund value, whichever is lower. This instant liquidity puts the liquid fund on par with a savings account. These funds can also be used when staggering investment into an equity fund using the systematic investment plan (SIP). It allows you to fetch a higher return compared to using a savings account to transfer the money.

The bread and butter portion of the bond portfolio should be in a low or short duration fund, says Kaustubh Belapurkar, Director, Fund Research, Morningstar Investment Advisor. These will invest in instruments with duration up to three years, and are suitable for investors looking to park money over a similar time horizon. These are not too exposed to interest rate risk as they carry low duration in their portfolio, yet are able to capture slightly higher return compared to a liquid fund.

Amol Joshi, Founder, PlanRupee Investment Services, says, “These funds provide the best of both worlds—yielding slightly better return while largely keeping volatility at bay.” For most investors, this combination of liquid fund and low duration fund is enough to fill the bond fund basket. Their returns are least affected by the changing interest rate scenario and carry little default risk.

Other categories of bond funds, however, require a deeper understanding of interest-rate risk, duration calls and credit risk. But if investors are keen on slightly higher return, then experts suggest rounding off the debt fund portfolio with a small allocation to a credit risk fund or even a dynamic bond fund. A credit risk fund generates higher returns by targeting lower rated corporate bonds carrying a higher coupon rate.

Currently, with corporate earnings recovery on the horizon, there is a higher possibility of lower rated paper getting upgraded, which can boost the returns from a credit risk fund. However, funds with poor credit profile can take a hit if companies default on loan repayments.

For the risk takers, a dynamic bond fund can provide another tactical play on interest rates. It attempts to capture higher return by aggressively shifting the portfolio between short and long duration according to expected movement in interest rates. Theoretically, these are ideal for investors who don’t have the understanding to take a call on interest movements. Yet, most dynamic bond funds have failed to live up to the billing and have often been caught on the wrong foot, hurting fund returns.

Other categories such as medium duration, long duration, corporate bond, banking and PSU fund, among others, can be safely ignored as they usually do not add much value to the lay investor’s portfolio.

End of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- Kolkata actor lodges complaint over 'kiss without consent'; innocent, says director

- ACT Hockey: India hammer Malaysia 8-1

- Six takeaways from US debate where Kamala ‘trapped’ Trump

- An Indian, not Columbus, found America, says MP education minister

- Malaika Arora's father Anil Arora dies by suicide

- Encounter breaks out between security forces and terrorists in Udhampur

- Why growing lure of protein supplements is worrying health experts

- Apple announces price cut on iPhone 15, iPhone 14 models: New prices

- Musk’s offer to ‘give child’ to Swift sparks outrage: ‘How low can one go?’

- Kejriwal's custody extended till Sept 25, bail granted to Durgesh Pathak

Popular Categories

Hot on the Web

Top Trends

Trending Topics

Deepika PadukoneMalaika Arora Father DeathArbaaz KhanJayram RaviAishwarya Rai BachchanSlat WaterWeight GainGOAT CollectionVikas Sethi DeathMalayalam ProducersIndia's Best Dancer 4Simi GarewalDilli BabuIndian National ParksLaung BenefitsVikas SethiiPhone 16Dubai Princess Sheikha MahraMG Windsor EvWordle Answer

Living and entertainment

Latest News

Manju Warrier expresses gratitude for birthday wishes: "Forever humbled and grateful"Haryana HPSC PGT admit card 2024 out at hpsc.gov.in: Direct link to download hall ticket here6,0,6,6,6 - Smashing Kieron Pollard rolls back the clock in Caribbean Premier League - WatchRelief for Amul in trademark war against Italian brandAfghanistan vs New Zealand: Why is Greater Noida stadium hosting a Test match?Shilpa Shetty and Raj Kundra spotted at the Siddhivinayak Temple; video insideDonald Trump and Kamala Harris shake hands as they meet for first time on debate stage: Watch the 'awkward' momentPrince William’s commitment to a lasting marriage with KateWhen Jaya Bachchan revealed she had a huge crush on Dharmendra, called him a 'Greek God' in front of Hema MaliniJr NTR starrer 'Devara: Part 1' completes censorship formalities; receives UA certificateGeorgia school shooting: Suspect's mom's call wasn't the only alert, multiple warnings overlooked before Apalachee high attack'Trump should not be telling a woman what to do with her body', says Kamala Harris on abortion rights during US presidential debateArbaaz Khan spotted outside Malaika Arora's house along with police after the tragic news of her father's demise by alleged suicide - WATCH VIDEOShivaji statue collapse: Sculptor’s custody extended till September 137 Common veggies that are loaded with iron and essential nutrientsBengaluru techie pockets 1k cryptocurrencies of his company, lands in police netThe Luckiest Zodiac Signs: Who's Got the Midas Touch?When Malaika Arora missed her father Anil Arora and the whole family during Covid - a memory set in monochrome

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service