- News

- Business News

- India Business News

- India Business News

- Reduced annuity returns after rate cuts: LIC chief

Trending

Reduced annuity returns after rate cuts: LIC chief

LIC's new MD & CEO, R Doraiswamy, outlines strategies to maintain market leadership amid evolving financial landscapes. The insurer is balancing par and non-par products, adapting to regulatory changes, and strategically evaluating opportunities in the health sector. While government stake dilutions are anticipated, LIC aims for sustainable growth and profitability, focusing on long-term value creation.

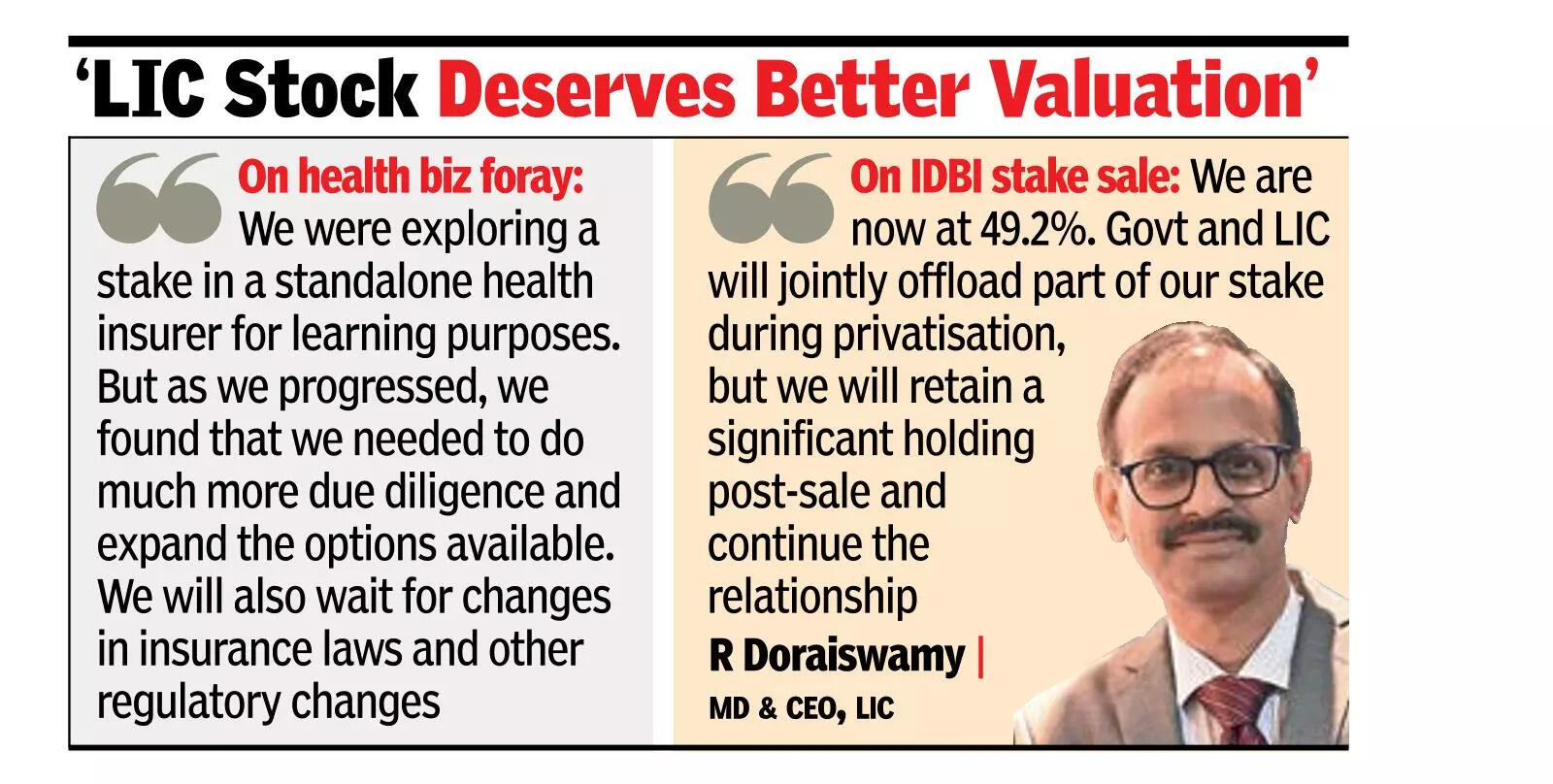

LIC’s share price is below the IPO price. How will you attract investors if the govt wants to dilute? What’s your dividend policy?

We believe LIC deserves a better valuation. Govt is closely watching the market and certainly will take a call on a price only when there is enough scope in the market to go for further dilution. They aim to reduce their holding to 90% by 2027 and are working toward that. Dividend distribution will depend on capital and solvency needs. We currently have a solvency ratio above 2, while the requirement as a systemically important insurer is 1.75. The solvency ratio will drop by a few basis points once the regulator implements risk-based capital requirements and IFRS (accounting norms). We’ve engaged Deloitte as consultants and are preparing for compliance.Is LIC moving toward more profitable products? Why was there a drop in the number of policies?

We’ve shifted towards non-par products to match market demand, especially from younger customers seeking guaranteed and short-term plans. Our non-par share in premiums has risen from 7% in 2022 to 30% now. We will now balance focus between par and non-par products. The decline in policies was because a new master circular in Oct 2024 required us to modify all products, increase the minimum sum assured, and change commission structures. This reduced policy numbers, especially in popular low-ticket plans. We saw a significant degrowth in the number of policies sold during Q3FY25, which continued in Q4 as well as Q1FY26. We’re working to recover growth in the second half.There was news about LIC picking up a stake in a health insurer. When will the deal conclude? Will you look at doing composite (life and non-life) insurance?

We never named any company. We’re exploring taking a strategic stake in a standalone health insurer for learning purposes. But as we progressed, we found that we needed to do much more due diligence and expand the options available, examining them in greater depth. So we decided not to make a quick move. We will also wait for changes in insurance laws and other regulatory changes expected in the near future. We have been a pure life insurer since 1972. We’ll examine the composite option if laws change, but we have no such plan now.What’s the aspiration in banking after the IDBI stake sale proposal?

Our vision is to be a transnationally competitive financial conglomerate. We acquired up to 51% of IDBI Bank because their recapitalization need provided us an opportunity. We are now at 49.24%. The govt and LIC will jointly offload part of our stake during privatization, but we will retain a significant holding post-sale and continue the relationship.LIC had announced digital initiatives. How will that impact agency distribution?

Our programme DIVE (Digital Innovation and Value Enhancement) is about fully digitalizing customer and intermediary services. The Jeevan Samarth initiative focuses on agency transformation—training and equipping agents with technology for higher productivity and retention. We are looking at strengthening our agency, which is our major strength, equipping them with technology and training so they can perform at a higher level. We’ll maintain both full- and part-time agents, training them to evolve into wealth advisors.Do you plan to grow your market share?

The focus of the government is to allow 100% foreign direct investment so that there are new players. When the market has more players, market share may reduce. We are not looking at market share as a prime focus. We are focusing on continuing to grow sustainably and profitably while expanding the market.Stay informed with the latest business news, updates on bank holidays, public holidays, current gold rate and silver price.

End of Article

Follow Us On Social Media

Hot Picks

Top Trending

Tired of too many ads?go ad free now

Trending Stories

In Business

Entire Website

- China lifts rare earths export curbs: India’s electronics sector could benefit from relaxations – what industry experts have to say

- Stock market today: Nifty50 opens in red; BSE Sensex down over 100 points

- Top stocks to buy today: Stock recommendations for August 22, 2025 - check list

- RBI seeks debate on inflation targets

- Sebi looks to promote long-tenure derivatives

- VC stakes at risk, startups look at rejigging biz models

- Air India cuts loss but AI Express sees it rising

- GST cut to help customers, impact on industry unclear

- 'Terror support seen in operations of gaming companies'

- SUV, sedan prices likely to see sharp cut, with lower 40% GST

- “The way her face changed”: Taylor Swift’s expression in a new resurfaced clip with Travis Kelce has made fans emotional

- 'Cracker Barrel goes woke': CEO under MAGA fire for changing logo first time in 48 years, removes 'white guy'

- USCIS tightens the age-out noose on H-1B kids: How this rule change could derail their college dreams

- Pakistan SC grants bail to Imran Khan in May 9 cases, but ex-PM stays in jail

- Indian student arrivals to US crash 46% in July: Here’s how it could cost American students

- “It’s a war”: Wayne Gretzky’s legacy came under fire amid Donald Trump’s controversial trade war with Canada

- Trump admin reviewing 55 million visas: Focus on deportable offences; 6,000 student visas already revoked

- Horoscope Tomorrow, August 22, 2025: Ketu can cause emotional detachment for these zodiac signs tomorrow

- Taylor Swift and Travis Kelce spark engagement buzz as fans anticipate big anniversary announcement

- Patrick Mahomes opens up on father’s DWI arrest and reveals how the incident deeply impacted his family

Financial calculators

Tired of too many ads?go ad free now

Explore Every Corner

Across The Globe

Wayne GretzkyRoblox shutdownAndy RoddickTyson BagentVanessa BryantTVK chief VijayShubhanshu ShuklaBangalore traffic finesRahul DravidJanel GrantCora JadeGautam GambhirSachin TendulkarDr. James DobsonEric AdamsVillanova University shootingUS Truck Driver VisaAlina HabbaRahul GandhiS JaishankarChinaTej Pratap YadavColorado dairy accidentAlligator AlcatrazWashingtonUSAID ClaimBSNLChina ExportDelhi Stray DogsUS Visa Holder

Hot on the Web

Magnesium Deficiency SymptomsHeart AttackDhanashree VermaHigh Blood Sugar SymptomsElvish YadavBeautiful Pet BirdsColon Cancer SymptomsUSFDA Cookware WarningVitamins For Hair GrowthBelly Fat LossShah Rukh KhanLiver HealthKidney HealthOzempic Vulva Side EffectsAkshay KumarCoolie Vs War 2Hair RegrowthBrain-Eating Amoeba SymptomsMillie Bobby BrownOveractive Bladder SymptomsRajesh KhannaAngelina JolieYuzvendra ChahalKapil SharmaRajnikanthGauri KhanTaj Mahal Restricted ChambersWar 2 Box Office CollectionCoolie Movie ReviewCoolie Box Office CollectionOvercrowded Tourist DestinationsAshwagandha For MenHigh Protein FoodsKidney Stone PainHigh Cholesterol SymptomsLakshman BootiColorectal CancerOral SymptomsReduce Face Fat DietSide Effects Of BananasGinger Tea Side EffectsKidney Damage Symptoms

Trending Topics

Online Gaming BillDhanashree VermaBabar AzamHTET ResultGATE 2026IBPS Clerk 2025 RegistrationIndian Students in USAWho is DR Pooshan MohapatraMBBS and PG Seats in IndiaSara ErraniNHL Trade RumorsConnor BedardAuston MatthewsRyan GarciaJohn CenaUndertakerCalifornia SchoolsUS Education DepartmentMarco RossiChhattisgarh Man KilledMumbai BEST Election ResultAhmedabad Student MurderRekha Gupta Attack CaseJaswinder BhallaAhmedabad School MurderElvish Yadav House Firing CaseSimone TataMahisagar Student StabbingBengaluru Bike TaxiKarnataka E ChallanMustafa SuleymanEpic CEO FaulknerCoconut Water For Kidney PatientsApple iPhone 17Bill GatesIBM and NASA Unveil SuryaKairan QuaziNyt ConnectionsStarlink To Use AadhaarOpenai Cfo Sarah FriarGoogle Pixel 10 Pro FoldWordle Today

Popular Categories

HeadlinesSports NewsBusiness NewsIndia NewsWorld NewsBollywood NewsHealth+ TipsIndian TV ShowsTechnologyTravelEtimesHealth & FitnessNFLAugust Long Weekend 2025India vs EnglandAstrologyWeather TodayPlatinum Rate TodaySilver Rate TodayGold Rate TodayIs Bank open todayIs Bank Open TomorrowBank Holidays in AugustPublic Holidays in AugustStock Market HolidaysFinancial CalculatorsTechnology NewsInternational SportsPublic HolidaysBank Holidays

Latest News

Shani Amavasya 2025: Donate these items to get rid of Saturn's malefic effectsNumerology horoscope today, August 22, 2025: What your name's first letter reveals todayNCR embraces DIY Ganpati workshops for sustainable celebrationsRanthambore horror moment: Tourists left stranded in the jungle after canter breaks down—key safety lessonsDelhi CM Rekha Gupta resumes public meetings two days after assault; police probe widensWho was Dr. James Dobson? 'Focus on the Family' founder dies at 89; was adviser to five US presidentsSudden cardiac arrest: Why survival rates depend on bystanders like youBiggest expansion: 14km of new metro tracks, a giant leap for KolkataHybrid security: CISF trains private guards at smaller ports; focus on threat identification, emergency responseGhaziabad: FIR against YouTuber Puneet Superstar for calling Mayawati ‘mummy’ in video; triggers outrage among BSP supportersSend back your engineers to China with immediate effect: iPhone maker Foxconn gets instructions as iPhone 17 launch nears‘Karam’ trailer: Vineeth Sreenivasan surprises fans with dark thriller; Noble steps into action-hero avatarBabar Azam hits the nets following Asia Cup, PCB central contract snub - WATCHDid Tyla COLLAPSE at Brazil party? Video of bodyguard carrying 'Water' singer to car sparks concernHaryana shocker: 46-year-old man found dead by roadside; had brawl with neighbour hours earlier, probe onOpenAI plans India debut, set to launch 1st office in DelhiSwara Bhasker REACTS to social media backlash over sexuality and identity remarks; updates her X bio to 'Girl crush advocate'Indo-Korean center in Pune designated as official TOPIK test center for Korean language learners

Copyright © 2025 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service