- News

- Business News

- India Business News

- Inflation likely to fall this year but expect repo rate to touch 6.75% by April: Goldman Sachs

Trending

This story is from February 9, 2023

Inflation likely to fall this year but expect repo rate to touch 6.75% by April: Goldman Sachs

The brokerage expects the recent sharp drop in wholesale price inflation to feed into Consumer Price Inflation (CPI fuel) and CPI core goods inflation with a lag.

Representational Image

India's retail inflation is expected to fall to 5.5 percent in calendar year 2023, from an estimate of 5.8% earlier, driven by a dip in vegetable inflation, Goldman Sachs said in a report.

The brokerage expects the recent sharp drop in wholesale price inflation to feed into Consumer Price Inflation (CPI fuel) and CPI core goods inflation with a lag.

In the first half of calendar year 23, Goldman Sachs has revised headline CPI inflation forecast lower to 5.8% year on year (from 6.3% yoy earlier), mainly driven by lower food and fuel inflation, partially offset by higher core goods inflation.

It expects CPI inflation to remain just above the RBI’s target band in the first quarter of CY23 driven by high core services inflation and a reversal of the recent decline in vegetable prices. "From Q2 CY23 onwards, we expect headline inflation to come in below the upper end of the RBI’s target band of 6% yoy," said Santanu Sengupta, economist at Goldman Sachs.

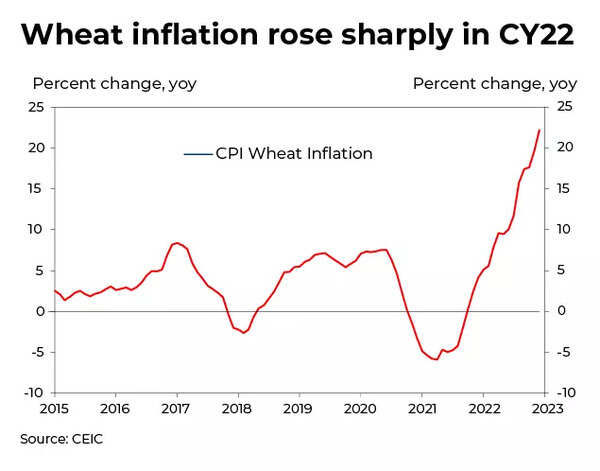

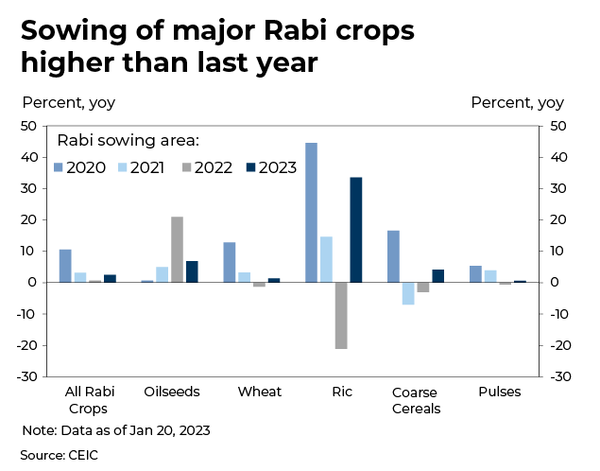

Wheat: Going forward, wheat prices are likely to moderate given higher sowing of wheat in the Rabi (winter) season due to good rainfall progress, conducive weather conditions in the last two months, which is likely to augur well for the upcoming wheat harvest season, and open market sale of wheat by the government from the stocks held by the Food Corporation of India.

Consequently, Goldman expect cereals inflation to moderate to 11.5% yoy in H1 CY23 and further to 6.6% yoy in H2 CY23.

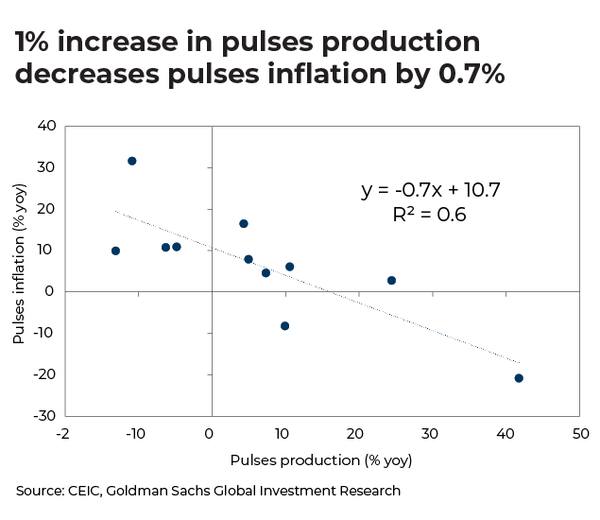

Pulses: Goldman estimates that a 1% increase in pulses production decreases pulses inflation by 0.7%. Sowing of pulses in Rabi (winter) season has seen good progress overall and is tracking higher than last year, which is likely to augur well for pulses production. Considering the same, we now forecast lower pulses inflation of 5.3% yoy (avg) in CY23 (vs. avg. 10.4% yoy earlier).

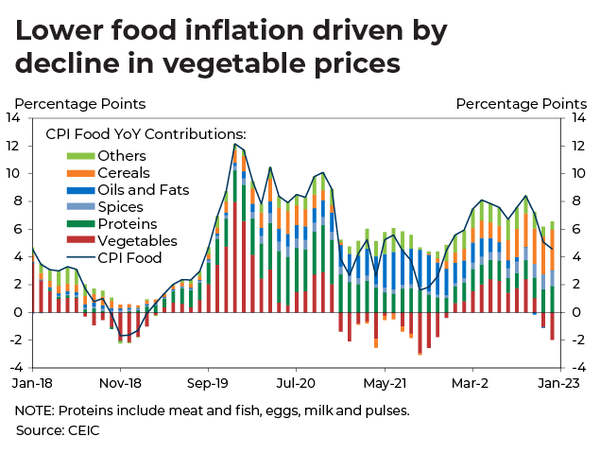

Vegetables and fruit: Food inflation in Q4 CY22 dropped sharply, solely driven by the larger than anticipated fall in vegetable (-11.6% QoQ SA) and fruit (-2.3% QoQ) prices. This trend has continued in January 2023 and in the first week of February.

Lower fuel Inflation

Goldman Sachs expects brent crude oil prices to rise above $100/bbl by Q3 2023; however, it has baked in some discount representing likely cheaper oil imports from Russia. Typically, wholesale (WPI) fuel inflation feeds into retail (CPI) fuel inflation with a lag.Going forward, it has lowered its fuel inflation forecast to 8.4% yoy in H1 CY23 (vs. 12.2% yoy earlier) and to 5.5% yoy in H2 CY23 (8.1% yoy earlier).

Sticky core services inflation

Core goods inflation is expected to be slightly higher at 6.2% yoy (vs. 6.1% yoy earlier). WPI inflation, which had remained elevated, dropped sharply to a 22-month low of 4.9% yoy in December.Goldman Sachs analysis suggests that WPI inflation feeds into core goods inflation with a lag of two quarters, which should cause core goods inflation to decline in H2 CY23. For the full year CY23, it forecast core goods inflation at 5.3% yoy (vs. 5.4% yoy earlier)

earlier).

Even Reserve Bank of India governor Governor on Wednesday stated that “stickiness of core inflation” is a matter of concern and that the pass through of input costs to core services is likely to keep core inflation elevated.

"Looking ahead, while inflation is expected to moderate in 2023-24, it is likely to rule above the 4 per cent target. The outlook is clouded by continuing uncertainties from geopolitical tensions, global financial market volatility, rising non-oil commodity prices and volatile crude oil prices. At the same time, economic activity in India is expected to hold up well. The rate hikes since May 2022 are still working their way through the system. On balance, the MPC was of the view that further calibrated monetary policy action is warranted to keep inflation expectations anchored, break the persistence of core inflation and thereby strengthen the medium-term growth prospects," said RBI Governor Shaktikanta Das.

The outlook on Inflation

The outlook for inflation is mixed, according to RBI. Prospects for the rabi crop have improved, especially for wheat and oilseeds, risks from adverse weather events remain but global commodity price outlook, including crude oil, is subject to uncertainties on demand prospects as well as from risks of supply disruptions due to geopolitical tensions.

Commodity prices are expected to face upward pressures with the easing of Covid-related mobility restrictions in some parts of the world. The Reserve Bank’s enterprise surveys point to some softening of input cost and output price pressures in manufacturing. Taking into account these factors and assuming an average crude oil price (Indian basket) of US$ 95 per barrel, RBI has projected inflation at 6.5 per cent in 2022-23, with Q4 at 5.7 per cent. On the assumption of a normal monsoon, CPI inflation is projected at 5.3 per cent for 2023-24.

Goldman Sachs continues to expect the RBI to hike 25bp further in the April meeting, on sticky core inflation and a reversal in vegetable prices, which would take the peak repo rate to 6.75% by April-2023.

The brokerage expects the recent sharp drop in wholesale price inflation to feed into Consumer Price Inflation (CPI fuel) and CPI core goods inflation with a lag.

In the first half of calendar year 23, Goldman Sachs has revised headline CPI inflation forecast lower to 5.8% year on year (from 6.3% yoy earlier), mainly driven by lower food and fuel inflation, partially offset by higher core goods inflation.

For the second half of the year, it has lowered its headline CPI inflation forecast to 5.3% yoy (from 5.5% yoy earlier), mainly driven by lower fuel and core goods inflation.

It expects CPI inflation to remain just above the RBI’s target band in the first quarter of CY23 driven by high core services inflation and a reversal of the recent decline in vegetable prices. "From Q2 CY23 onwards, we expect headline inflation to come in below the upper end of the RBI’s target band of 6% yoy," said Santanu Sengupta, economist at Goldman Sachs.

Here is why food inflation is likely to dip by 40 basis points in the first half of calendar year 2023:

Wheat: Going forward, wheat prices are likely to moderate given higher sowing of wheat in the Rabi (winter) season due to good rainfall progress, conducive weather conditions in the last two months, which is likely to augur well for the upcoming wheat harvest season, and open market sale of wheat by the government from the stocks held by the Food Corporation of India.

Consequently, Goldman expect cereals inflation to moderate to 11.5% yoy in H1 CY23 and further to 6.6% yoy in H2 CY23.

Pulses: Goldman estimates that a 1% increase in pulses production decreases pulses inflation by 0.7%. Sowing of pulses in Rabi (winter) season has seen good progress overall and is tracking higher than last year, which is likely to augur well for pulses production. Considering the same, we now forecast lower pulses inflation of 5.3% yoy (avg) in CY23 (vs. avg. 10.4% yoy earlier).

Vegetables and fruit: Food inflation in Q4 CY22 dropped sharply, solely driven by the larger than anticipated fall in vegetable (-11.6% QoQ SA) and fruit (-2.3% QoQ) prices. This trend has continued in January 2023 and in the first week of February.

Lower fuel Inflation

Goldman Sachs expects brent crude oil prices to rise above $100/bbl by Q3 2023; however, it has baked in some discount representing likely cheaper oil imports from Russia. Typically, wholesale (WPI) fuel inflation feeds into retail (CPI) fuel inflation with a lag.Going forward, it has lowered its fuel inflation forecast to 8.4% yoy in H1 CY23 (vs. 12.2% yoy earlier) and to 5.5% yoy in H2 CY23 (8.1% yoy earlier).

Sticky core services inflation

Core goods inflation is expected to be slightly higher at 6.2% yoy (vs. 6.1% yoy earlier). WPI inflation, which had remained elevated, dropped sharply to a 22-month low of 4.9% yoy in December.Goldman Sachs analysis suggests that WPI inflation feeds into core goods inflation with a lag of two quarters, which should cause core goods inflation to decline in H2 CY23. For the full year CY23, it forecast core goods inflation at 5.3% yoy (vs. 5.4% yoy earlier)

earlier).

Even Reserve Bank of India governor Governor on Wednesday stated that “stickiness of core inflation” is a matter of concern and that the pass through of input costs to core services is likely to keep core inflation elevated.

"Looking ahead, while inflation is expected to moderate in 2023-24, it is likely to rule above the 4 per cent target. The outlook is clouded by continuing uncertainties from geopolitical tensions, global financial market volatility, rising non-oil commodity prices and volatile crude oil prices. At the same time, economic activity in India is expected to hold up well. The rate hikes since May 2022 are still working their way through the system. On balance, the MPC was of the view that further calibrated monetary policy action is warranted to keep inflation expectations anchored, break the persistence of core inflation and thereby strengthen the medium-term growth prospects," said RBI Governor Shaktikanta Das.

The outlook on Inflation

The outlook for inflation is mixed, according to RBI. Prospects for the rabi crop have improved, especially for wheat and oilseeds, risks from adverse weather events remain but global commodity price outlook, including crude oil, is subject to uncertainties on demand prospects as well as from risks of supply disruptions due to geopolitical tensions.

Commodity prices are expected to face upward pressures with the easing of Covid-related mobility restrictions in some parts of the world. The Reserve Bank’s enterprise surveys point to some softening of input cost and output price pressures in manufacturing. Taking into account these factors and assuming an average crude oil price (Indian basket) of US$ 95 per barrel, RBI has projected inflation at 6.5 per cent in 2022-23, with Q4 at 5.7 per cent. On the assumption of a normal monsoon, CPI inflation is projected at 5.3 per cent for 2023-24.

Goldman Sachs continues to expect the RBI to hike 25bp further in the April meeting, on sticky core inflation and a reversal in vegetable prices, which would take the peak repo rate to 6.75% by April-2023.

End of Article

FOLLOW US ON SOCIAL MEDIA

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- Last spoke to family 3 days ago: Kerala man linked to Hezbollah pager blasts?

- 'Offered water laced with drugs': 13-yr-old Dalit gang-raped in car

- How Israel killed most wanted terrorist with a phone call in 1996

- Watch: Army troops show night ops skills in Ladakh’s high-altitude areas

- 1st Test Live: Pant, Shubman slam fifties vs Bangladesh

- Speaks 7 languages, PhD holder: All about the woman linked to pagers blast

- Sri Lanka is not voting for a new president. It's voting for...

- EY employee's death: Anna Sebastian's father appeals to the company

- PM Modi on 3-day US visit for Quad summit: Key agenda, full schedule

- Cheeky Pant helps Bangladesh set field on Day 3 of Chennai Test

Popular Categories

Hot on the Web

Top Trends

IND vs BAN Live ScoreRohit SharmaVirat KohliRishabh PantUGC NET Result 2024Cristiana Barsony ArcidiaconoTirupati Laddu RowIsraeli Strikes on HezbollahRhea RipleyIsrael Hezbollah WarIND vs BAN Highlights Days 2Kerala Lottery ResultTirupati PrasadamEY Pune EmployeeSean DiddySandip GhoshLive Cricket Score

Trending Topics

Stree 2 CollectionRuksana BanoAbdu RozikYudhra ReviewJayamSana Khan HusbandTirupati Laddoo ControversyGOAT CollectionVaazha OTT ReviewKozhipannai Chelladurai ReviewCheetahsKangana RanautAditi Rao HydariDalljiet KaurHoliday DestinationVikas SethiBest Selling Earbuds Under 1000Apple iPhone 16 ProVirat KohliWordle Answer

Living and entertainment

Latest News

Stuck in Lebanon for 23 years, Punjab man back homeVivek Ramaswamy hints at Ohio governor run at his Springfield town hallRoman Reigns Gives His Word to Back Cody Rhodes Against The BloodlineSupreme Court questions change in NEET-PG pattern, seeks response of NBE and CentreYudhra box office collection day 1: Siddhant Chaturvedi and Malvika Mohanan starrer opens with Rs 4.50 croreBigg Boss fame Sana Khan on her photos wearing Abayas going viral during her Maldives vacation; says 'people think you can only wear swimwear...'UP man kills newborn daughter in fit of rage over fourth girl cild, ArrestedSalesforce to expand its innovation hubs in Bengaluru, HyderabadThe truth about sugar substitutes: Safe alternative or hidden health risk?Govt caps late fee at Rs 1k for vehicle fitness certificateSalman Khan will NOT make a cameo in Rohit Shetty’s 'Singham Again'; fans say 'disappointed'Not taking EY to court, says dead CA's fatherCheeky Rishabh Pant helps Bangladesh set field on Day 3 of Chennai Test - WatchKarnataka HC asks couple to seek spiritual guru's help to save marriageBombay HC strikes down Centre's fact check unitFire breaks out at furniture market in Central DelhiLibra, Daily Horoscope Today, September 21, 2024: Focus on a balanced diet and exercise to maintain well-beingMemeFi daily codes for 21 September 2024: Boost your earnings with daily codes and know how to maximize

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service