- News

- Business News

- India Business News

- Despite caution of economic downturn life style spending continues unabated

Trending

This story is from October 25, 2013

Despite caution of economic downturn life style spending continues unabated

With confidence in the economy’s ability to rebound swiftly remaining low, plans for discretionary spends on ultra high value spends like boats and aircrafts saw a decline.

Real estate, continued to retain its flavour. However, with confidence in the economy’s ability to rebound swiftly remaining low, plans for discretionary spends on ultra high value spends like boats and aircrafts saw a decline. These were the findings of a report – “Top of the Pyramid 2013: Decoding the Ultra HNI-India” (T.O.P. 2013 Report) brought out by Kotak Wealth Management & CRISIL Research.

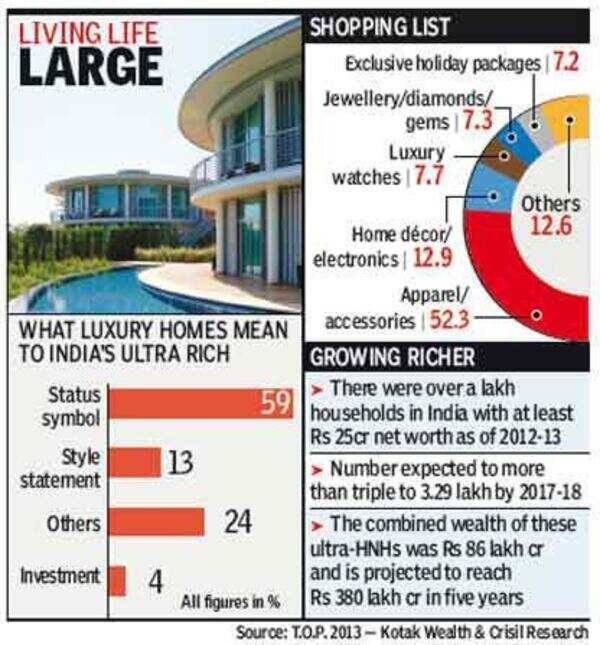

“If we consider a household with a minimum net worth of Rs 25 crore, there are more than a lakh ultra high net worth households in India as of 2012-13. This figure is poised to more than triple to over 3.29 lakh households by 2017-18,” according to the T.O.P. 2013 Report. The total net worth of this segment is also expected tor each Rs. 380 lakh crore in 2017-18 from a current estimate of Rs. 86 lakh crore.

Interestingly non-metro houses almost half of ultra-high net worth individuals (HNIs). While 54% of the ultra HNIs are currently based in the metros, 13% are concentrated in the top six cities of Bangalore, Ahmedabad, Pune, Nagpur, Hyderabad and Ludhiana. In the long run, these numbers will change in favour of non-metros.

“Making the most of even relatively bad times, getting wealthier each day and living life to the hilt, that is the Indian ultra HNI for you, circa 2013” cites the T.O.P. 2013 Report.

The good news for the luxury market segment is that ‘life-style’ spending has not gone out of fashion. This report examined the spending patterns of India’s ultra rich during 2012.

Apparel and accessories dominated this spend at 53%, followed by home décor and electronics at 12.9% and luxury watches at 7.7%. Further the number of ultra HNIs who shop in India even for global luxury brands is growing steadily. Vacation plans also remained unchanged, ultra HNIs travel overseas typically once or twice a year, and beaches were the most preferred location -

the choice of 22.7% of the respondents. Only 13% of the respondents said the downturn had impacted their vacation plans.

However, results of this survey, covering 150 ultra HNIs (interviews were conducted between March to May 2013), showed that compared to the previous year, more people postponed high-end discretionary purchases (such as private home theatres, top-end cars, yachts, aircraft etc) until they got a better sense of an economic recovery.

In a normal year, the discretionary to non-discretionary spend ratio is around 41:59; during a sustained downturn as in 2012, the Kotak Wealth-CRISIL survey found, this ratio changed to 33:67. Further, last year in terms of percentage terms, spending as a proportion of income was up nearly 6 percentage points to 28.3 per cent. Given the caution on discretionary purchases this year (spending during 2012 was considered); the proportion was 29.1 per cent (only a modest 1 percentage points rise).

The T.O.P. 2013 Report looked extensively at the luxury home segment, where location or the exclusivity that an address affords, was found to be the single most important factor driving ownership of a luxury home. For the right location, the ultra HNIs were willing to pay staggeringly more than market rates. To 58.6% of the respondents, a luxury home was a status symbol. Whisper marketing and exclusive invites were the means adopted by developers to tap the ultra rich. Ultra HNIs were also increasingly seen as purchasing luxury properties abroad in Singapore, London and Dubai. However, real estate planning business was found to be at a nascent stage in India and buying a luxury home continued to be a family decision.

It should be noted that Reserve Bank of India has via its circular in August 2013, prohibited overseas remittances for property purchases.

The defining finding of the 2013 survey report is that a large percentage of respondents believe that there is a downturn and early recovery is not in sight. Nearly 90 per cent of the respondents agreed that there is a slowdown. Of which the time line for recovery indicated by about 65 per cent varied from mid-2013 to mid-2014, with a bias towards the latter.

The silver lining was a gradual improvement in business confidence with majority of them ploughing back over 30% of their income into their primary business.

About the Author

Lubna KablyEnd of Article

FOLLOW US ON SOCIAL MEDIA

Photostories

Hot Picks

TOP TRENDING

Trending Stories

In Business

Entire Website

- Will banks open only for 5 days a week? Here’s what you should know about IBA’s proposal

- India set to be third largest economy, says S&P Global

- Dalal Street bull run continues! BSE Sensex crosses 69,000 for the first time; Nifty above 20,800

- Byju’s reduces notice period for employees as troubles mount

- Sensex surges over 900 points, Nifty above 20,550 as BJP state election wins bolster Modi's Lok Sabha 2024 prospects

- UltraTech to buy building materials business of Kesoram in 7,600 crore deal

- Tata Technologies stock debuts at a bumper 140% premium; share price at Rs 1200 on BSE

- Tata Technologies share allotment: How to check IPO allotment status, listing date, GMP

- BSE m-cap rides rally in Adani stocks, tops $4 trillion

- Charlie Munger, who helped Warren Buffett build Berkshire, dies at 99

- 'Very big achievement': PM Modi launches 3 PARAM Rudra supercomputers

- 'Sinister forces ...': VP Dhankhar raises red flag over rise in religious conversions

- What's making more and more NRIs invest in Indian real estate?

- Cong, Himachal govt firefight after minister announces 'UP-like' diktat for eateries

- Pune Porsche case: Police add forgery, corruption charges against teen

- Israeli PM Netanyahu orders 'full force' fight against Hezbollah

- Explained: Why SC wants to label ‘child pornography’ CSAEM

- Zerodha CTO Kailash Nadh: I have stopped using Google for….

- In big push, Centre increases minimum wage for workers

- Proactive heart care: How can knowledge and tools empower us?

Popular Categories

Hot on the Web

Top Trends

Trending Topics

Living and entertainment

Latest News

First person died in UK from ‘liquid’ Brazilian butt lift: All you need to know about liquid BBL and risks it poses8 Spices that can help reduce high blood sugarDiddy's Lawyer defends buying 1000 Bottles of baby oil to pass Homeland security raidsShankar to bring Chiyaan Vikram and Suriya together for a film on the Velpari novelThere’s plastic in your chai-samosa, and India is No. 1 culpritKerala lottery results: Karunya Plus KN-540 winners for 26 September 2024; first prize Rs. 80 lakhs, second prize Rs 10 lakh and third prize Rs. 1 lakhLeo, Daily Horoscope Today, September 26, 2024: Positive developments are expected in love lifeDelhi high court extends interim arrest protection for former IAS officer Puja Khedkar'I'm not upset with Kangana but ... ': Chirag Paswan as Mandi MP apologises for farm law remarkThe most important lesson investors can learn from trekkersChennaiyin FC eye second win on the trot in Indian Super LeagueTaliban could face Hague tribunal for their treatment of women and girlsCandidates Protest Outside JSSC Office, Accuse Malpractice in Recruitment Exam“The Chiefs get way more calls”: Rob Gronkowski says that the Chiefs gets more favorable calls than the PatriotsMaharashtra polls: Mumbai's Byculla & Versova seats are sticking points in MVA talksGmail app on Android and iOS is getting Google’s blue verification checkmarks: Here's how it'll affect usersTop 5 WWE’s tallest wrestlers from Giant Gonzalez to The Great Khali'Bhool Bhulaiyaa 3' new poster: Kartik Aaryan reveals 'Rooh Baba Vs Manjulika' face off

Copyright © 2024 Bennett, Coleman & Co. Ltd. All rights reserved. For reprint rights: Times Syndication Service